Adulting, Made Easier – Stories & Straight Talk

Quick reads, helpful tips, and honest breakdowns of what you need to know.

Featured Posts

4 Year-End Tax-Saving Strategies For 2022

Although the end of the year can be a hectic time, it’s also the deadline for your family to implement a number of key tax-savings strategies. By taking action now, you can significantly reduce your tax bill due in April, but with just a few weeks left in 2022, you better act fast.

While there are dozens of potential tax breaks you may qualify for, here are 4 of the leading moves you can make to save big on your 2022 tax return. However, there may be other opportunities for saving, so meet with us, your Personal Family Lawyer® to make certain you haven’t missed a single one.

Trusts & Taxes: What You Need To Know

People often come to us curious — or confused — about the role trusts play in saving on taxes. Given how frequently this issue comes up, here we’re going to explain the tax implications associated with different types of trusts in order to clarify this issue. Of course, if you need further clarification about trusts, taxes, or any other issue related to estate planning, meet with us, your Personal Family Lawyer® for additional guidance.

3 Critical Considerations For How To Save For Your Child’s (or Grandchild's) College Education—Part 2

Last week, in part one of this series, we discussed 529 plans and education savings accounts, which are both popular options for saving for a college education. One of the main reasons for their popularity is their tax-saving advantages. The money you contribute to a 529 account grows on a tax-deferred basis, and withdrawals are tax-free, provided they are used for qualified education expenses, such as tuition, room and board, and other education-related fees.

That said, one of the downsides of 529 plans is that they come with strict limits on how you can use the funds (for education-related expenses only), and they also have a limited range of options for how you can invest your funds, primarily in various mutual funds. For these reasons, 529 plans and ESAs aren’t always the best fit for some families looking to save for their loved one's education.

3 Critical Considerations For How To Save For Your Child’s (or Grandchild's) College Education—Part 1

If you have started to save for your child or grandchild’s college education, it’s worth considering whether to use a 529 plan, an education savings account, or an Irrevocable Trust.

Here’s what we think you should consider as you decide:

First, consider whether you want your offspring to have broader options than just the traditional college experience.

Since the pandemic's start, college enrollments have declined by over one million students over the past two years. With college tuition getting more and more expensive, many students are considering alternatives to the traditional higher education path.

Start Planning Now to Prepare Your Estate for a Possible Democratic Sweep—Part 2

No matter who you vote for on November 3rd, you may want to start considering the potential legal, financial, and tax impacts a change of leadership might have on your family’s planning. As you’ll learn here, there are a number of reasons why you may want to start strategizing now if you could be impacted, because if you wait until after the election, it could be too late.

While we don’t yet know the outcome of the election, Biden could win and the Democrats could take a majority in both houses of Congress. If that does happen, a Democratic sweep would have far-reaching consequences on a number of policy fronts. But in terms of financial, tax, and estate planning, it’s almost certain that we’ll see radical changes to the tax landscape that could seriously impact your planning priorities. And while it’s unlikely that a tax bill would be enacted right away, there’s always the possibility such legislation could be applied retroactively to Jan. 1, 2021.

Start Planning Now to Prepare Your Estate for a Possible Democratic Sweep—Part 1

No matter who you are voting for on November 3rd, you may want to start considering the potential legal, financial, and tax impacts a change of leadership might have on your family’s planning. And as you’ll learn here, there are a number of reasons why you should start strategizing now, because if you wait until after the election, it will very likely be too late.

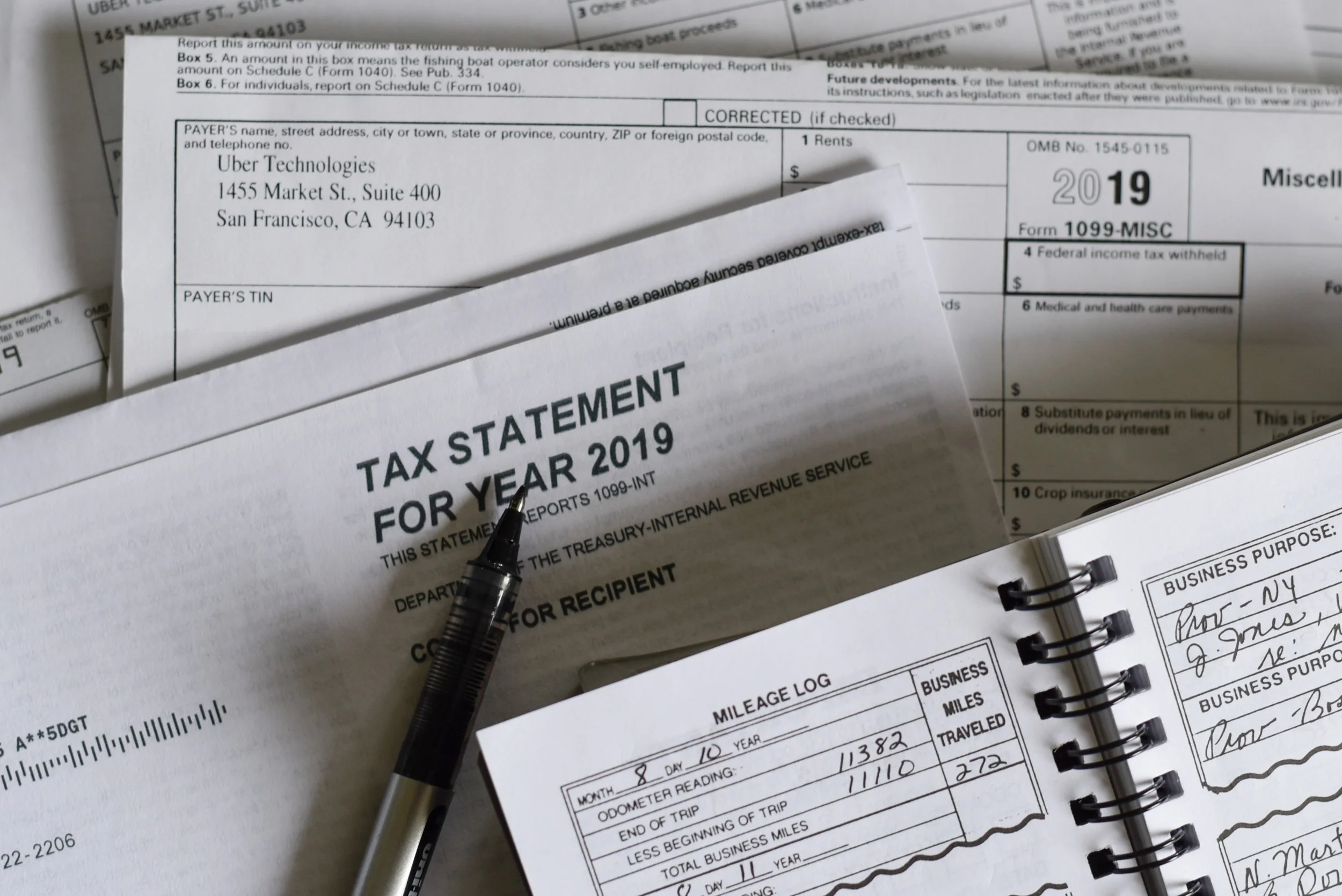

6 Changes to Watch For In Your 2020 Taxes

Although you may have just filed your 2019 income taxes in July, now is the time to start thinking about your 2020 return due next April. While it’s always a good idea to be proactive when it comes to tax planning, it’s particularly important this year.

In addition to annual updates for inflation, the Coronavirus Aid, Relief, and Economic Security (CARES) Act provides individual taxpayers with several new tax breaks, most of which will only be available this year. The sooner you learn about the different forms of tax-savings available, the more time you will have to take advantage of them.

Here are 6 ways your 2020 return will differ from prior years:

How Do Trusts Help You Save on Taxes?

Many people come to us curious (or confused) about trusts and taxes. So today’s article is going to sort it out and clarify things for you.

There are two types of trusts, and each have different tax consequences.

Revocable trusts, which are the far more commonly used trusts, have no tax consequences whatsoever. A revocable trust has your social security number as its tax identifier, and is not a separate entity from you for tax purposes.

When you have an irrevocable trust, either created during life, at death through a revocable living trust, or through a will that creates a trust, that trust has its own EIN, or employer identification number (also called a TIN or taxpayer identification number).